High-Yield Savings vs CDs vs Treasury Bills: 2026 Rate Comparison & Decision Matrix

You have cash sitting in a checking account earning 0.01% and you know you can do better. The question is which of the three serious options actually wins for your situation: a high-yield savings account, a certificate of deposit, or a U.S. Treasury bill. In May 2026 the headline rates are close enough that the decision turns less on yield and more on liquidity, taxes, and how certain you are about your timeline. This piece walks through the numbers with named institutions, the after-tax math state by state, and worked examples for $10,000, $50,000, and $100,000 cash positions.

The Three Vehicles, Briefly

A high-yield savings account (HYSA) is a federally insured bank deposit that pays a variable rate, usually with no minimum balance and same-day or next-day transfers via ACH. Top online banks have been paying within roughly 1.0-1.5 percentage points of the federal funds rate for the last several years. Coverage is up to $250,000 per depositor, per bank, per ownership category under the FDIC.

A certificate of deposit (CD) is a time deposit at a bank or credit union. You agree to leave your money for a fixed term (typically 3, 6, 9, 12, 18, 24, 36, 60 months) in exchange for a fixed rate locked at purchase. Early withdrawal incurs a penalty — usually 3-12 months of interest depending on the term and issuer. CDs carry the same FDIC insurance as savings accounts.

A U.S. Treasury bill (T-bill) is a short-term debt obligation of the federal government with maturities of 4, 8, 13, 17, 26, or 52 weeks. T-bills are sold at a discount to face value and pay no coupon — you buy a $1,000 bill for, say, $978.50 and collect $1,000 at maturity. They're backed by the full faith and credit of the U.S. government with no FDIC cap, and the interest is exempt from state and local income tax.

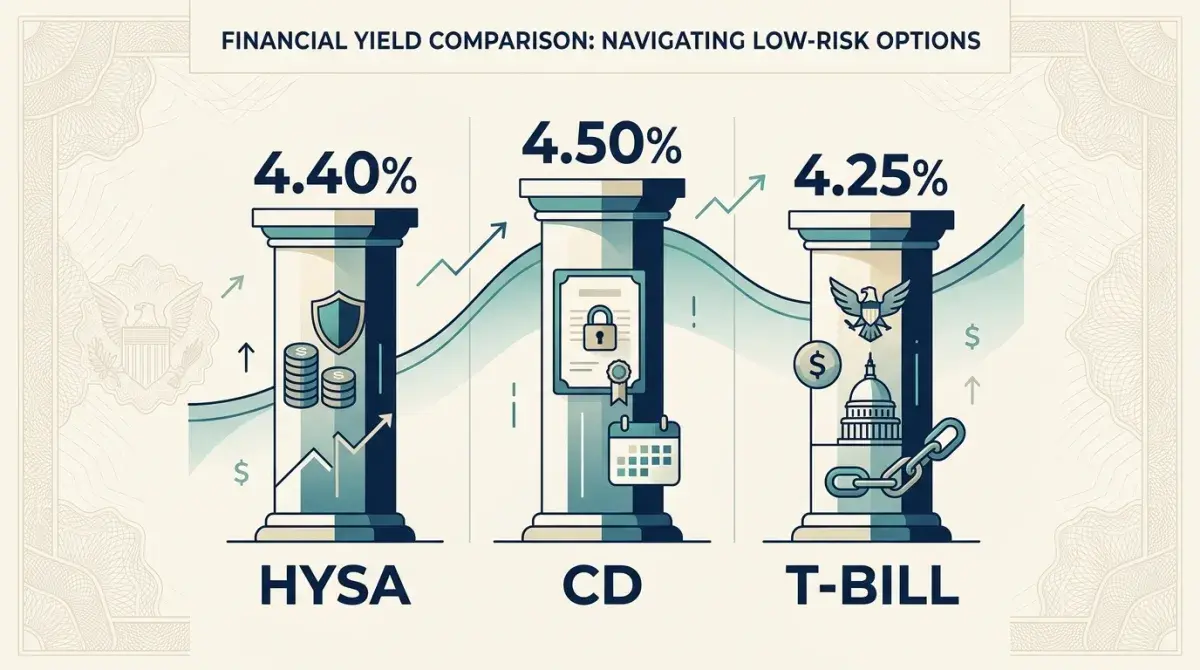

May 2026 Headline Rates: HYSA, CD, T-Bill

The table below shows representative rates from named institutions and from the U.S. Treasury as of mid-May 2026. Bank APYs change frequently — confirm the current rate at the source link before purchasing. Treasury bill yields come from TreasuryDirect auction results and the Federal Reserve H.15 release.

| Vehicle | Institution / Issuer | Term | Headline Yield (APY / Discount Yield) | Insurance / Backing |

|---|---|---|---|---|

| HYSA | Marcus by Goldman Sachs | On demand | ~4.40% APY | FDIC, $250K cap |

| HYSA | Ally Bank Online Savings | On demand | ~4.20% APY | FDIC, $250K cap |

| HYSA | SoFi Checking & Savings | On demand | ~4.50% APY (with direct deposit) | FDIC, $250K cap |

| CD | Discover Bank | 12 months | ~4.40% APY | FDIC, $250K cap |

| CD | Synchrony Bank | 12 months | ~4.50% APY | FDIC, $250K cap |

| CD | Capital One 360 CD | 9 months | ~4.30% APY | FDIC, $250K cap |

| T-Bill | U.S. Treasury (TreasuryDirect) | 13 weeks | ~4.25% (investment rate) | Full faith & credit of U.S. |

| T-Bill | U.S. Treasury (TreasuryDirect) | 26 weeks | ~4.30% (investment rate) | Full faith & credit of U.S. |

| T-Bill | U.S. Treasury (TreasuryDirect) | 52 weeks | ~4.15% (investment rate) | Full faith & credit of U.S. |

The headline spread between the best HYSA and the best CD is roughly 10-20 basis points. The spread between top HYSAs and 26-week T-bills runs around 10-25 basis points the other way. Before taxes, the three vehicles are within a quarter of a percent of each other. That changes once you factor in state income tax.

The State-Tax Wrinkle That Reshuffles the Order

Interest from HYSAs and CDs is fully taxable at the federal, state, and local level. Treasury bill interest is fully taxable federally but exempt from state and local income tax under 31 U.S.C. § 3124. For taxpayers in high-income-tax states, this exemption is worth real money. The table below converts a 4.25% T-bill yield into the equivalent fully-taxable yield a HYSA or CD would have to pay to net the same after-tax dollars, by state top marginal bracket.

| State (top marginal rate) | T-Bill Headline | Taxable-Equivalent Yield* | Annual Edge on $50K |

|---|---|---|---|

| California (9.3% bracket) | 4.25% | 4.69% | ~$220 |

| New York (6.85% bracket) | 4.25% | 4.56% | ~$155 |

| New Jersey (6.37% bracket) | 4.25% | 4.54% | ~$145 |

| Oregon (8.75% bracket) | 4.25% | 4.66% | ~$205 |

| Massachusetts (5.0% flat) | 4.25% | 4.47% | ~$110 |

| Illinois (4.95% flat) | 4.25% | 4.47% | ~$110 |

| Texas / Florida / TN / WA / NV (no income tax) | 4.25% | 4.25% | $0 |

*Taxable-equivalent yield = T-bill yield ÷ (1 − state marginal rate). Assumes you itemize at the federal level or take the SALT deduction up to the cap; for non-itemizers the effective state rate may be slightly higher. Confirm your specific bracket at the Tax Policy Center state rate table.

The conclusion is blunt: if you live in California, Oregon, Hawaii, Minnesota, New York, or New Jersey, a 4.25% T-bill beats a 4.50% HYSA on after-tax yield. If you live in a no-income-tax state, the T-bill exemption is worth nothing and you should choose on liquidity and convenience alone.

The Liquidity-vs-Yield Decision Matrix

Yield is one axis. Liquidity is the other. Here's how the three vehicles stack up across the factors that actually drive a decision.

| Factor | HYSA | CD | T-Bill |

|---|---|---|---|

| Access to funds | Same day / next day | Locked until maturity (penalty) | At maturity, or sell on secondary market |

| Early-exit cost | None | 3-12 months interest | Mark-to-market gain/loss only |

| Rate after Fed cut | Falls (variable) | Locked in | Locked in for term |

| Minimum purchase | $0-$1 typically | $0-$2,500 typically | $100 increments at TreasuryDirect |

| State / local tax on interest | Fully taxable | Fully taxable | Exempt (31 U.S.C. § 3124) |

| Insurance cap | FDIC $250K / bank / category | FDIC $250K / bank / category | No cap — direct U.S. obligation |

| Best for | Emergency fund, flexible cash | Known-date savings goals | Large balances, high-tax states, laddering |

Worked Example: $10,000 Emergency Fund

You have $10,000 you might need on a week's notice — car repair, medical bill, job loss bridge. This is unambiguously an HYSA decision. Put it in Marcus, Ally, SoFi, Discover, or any other top online savings account. At 4.40% APY, $10,000 earns roughly $449 in the first year with no risk of penalty if you have to pull it out at month 7.

Could you squeeze 10-15 extra basis points by laddering 4-week T-bills? Yes, and at $10,000 that's a difference of $10-15 a year. The hour you'd spend setting up TreasuryDirect and rolling the ladder is not worth $10. For emergency cash under $25,000, default to the HYSA and stop optimizing.

Worked Example: $50,000 House Down Payment in 14 Months

You're saving for a down payment, you signed an offer-letter timeline, and you know you'll close in roughly 14 months. The closing date is firm. The money cannot be at any market risk. This is the textbook CD use case.

- Synchrony 12-month CD at 4.50% APY: $50,000 earns $2,272 over 12 months, then sits in the funded account for the final two months. Total return: roughly $2,440. The rate is locked — if savings rates drop to 3.5% mid-year you're unaffected.

- Marcus HYSA at 4.40% APY: $50,000 earns roughly $2,565 over 14 months — but only if the rate holds. If the Fed cuts twice and the HYSA drops to 3.8% by month 8, real earnings come in closer to $2,200.

- 52-week T-bill at 4.15% (investment rate): $50,000 earns about $2,075 federally, but a California resident in the 9.3% bracket keeps an extra ~$190 in state tax savings, netting roughly $2,265 — competitive with the HYSA and locked in.

For a firm deadline of more than 6 months in a no-income-tax state, the CD wins on lock-in. In a high-tax state, the 52-week T-bill is within a hair of the CD with the bonus of FDIC-cap-free safety. Either is better than leaving it variable.

Worked Example: $100,000 Cash Bucket in California

You retired early, you keep three years of expenses in cash equivalents, and you live in California (9.3% marginal). This is where the T-bill story becomes loud.

| Strategy | Gross Yield | After CA State Tax | After-Tax $ on $100K |

|---|---|---|---|

| HYSA at 4.40% (Marcus) | 4.40% | 3.99% | $3,990 |

| 12-mo CD at 4.50% (Synchrony) | 4.50% | 4.08% | $4,080 |

| 26-week T-bill at 4.30% (rolled) | 4.30% | 4.30% (state-exempt) | $4,300 |

| T-bill ladder (4w-52w avg ~4.22%) | 4.22% | 4.22% (state-exempt) | $4,220 |

The rolled 26-week T-bill nets $220 more per year on every $100,000 than the HYSA and $220 more than the CD — without locking the money up beyond 6 months and without exposing balances above the $250,000 FDIC cap. For California, New York, and New Jersey residents holding six-figure cash buckets, the T-bill ladder is the default. For Texas, Florida, and Washington residents, the CD edges ahead.

Where to Actually Buy Each One

HYSAs open in 10 minutes online with two pieces of ID and an external account for funding. Look at the FDIC weekly national rate cap data to confirm you're being paid materially above the national average (currently around 0.4-0.6% — the spread you're hunting is 3.5+ percentage points above that).

CDs can be opened directly at any FDIC-insured bank or through a brokerage's “brokered CD” offering at Fidelity, Schwab, or Vanguard. Brokered CDs trade on a secondary market — meaning you can sell before maturity at market price — but they also carry interest-rate risk if you exit early. For pure park-and-forget money, direct bank CDs are simpler.

T-bills are purchased either directly at TreasuryDirect.gov with no fees, or through a brokerage account (Fidelity, Schwab, Vanguard) which also charges no commission on Treasuries. Brokerage purchase is easier to integrate into an existing portfolio; TreasuryDirect is the bare-metal option with no intermediary. Auction schedules and minimum bid sizes are published weekly.

Three Costs That Eat Into Your Real Yield

The headline APY is not what you keep. Three line items quietly compress the actual yield you receive on each vehicle. Knowing them is the difference between “I'm earning 4.5%” and “I'm actually netting 3.7%.”

1. CD early-withdrawal penalties. Discover charges 3 months of simple interest on terms under 12 months and 6 months on 12-24 month CDs. Synchrony charges 90 days on terms up to 12 months and 180 days on 13-48 months. A 6-month penalty on a 12-month CD at 4.50% paid out at month 7 wipes out roughly $1,125 of interest on a $50,000 deposit — turning a +4.50% commitment into a realized yield of roughly +1.6%. Read the penalty schedule before signing, not after.

2. Variable HYSA rate drift. A “4.40% APY” HYSA is not a contract. Banks reprice as the Fed moves and as their internal deposit costs shift. In the prior easing cycle several top HYSAs cut their headline rate four times in nine months, dropping from 4.50% to 3.40%. Check whether the bank reprices monthly or quarterly, and whether they offer a teaser rate that resets after 6 months. The FDIC national-rate cap data is the cleanest reference for spotting outlier banks.

3. T-bill reinvestment risk. A 13-week T-bill locks today's rate for 13 weeks. If you roll it and rates have fallen 50 basis points, your next quarter earns less. Laddering across 4, 8, 13, 17, 26, and 52-week maturities smooths this — at any given moment only a fraction of your balance reprices, so a sudden rate cut takes a year to fully flow through. The cost of laddering is administrative overhead: six positions, six maturity dates, and six reinvestment decisions per year.

What Happens If the Fed Cuts

The Federal Reserve's short-term policy rate sets the floor for everything in this article. As of mid-May 2026 the futures market is pricing roughly 50-75 basis points of cuts over the next twelve months. Here is how each vehicle responds.

- HYSA: Falls in sympathy, usually within 2-6 weeks of a Fed move. A 50 basis point cut typically translates into a 35-50 basis point cut in top HYSA APYs.

- CD (already opened): Unchanged. You locked the rate at purchase. New CDs at the same bank will price lower.

- T-bill (already held): Unchanged at maturity (face value is fixed). The secondary-market price of your bill actually rises when rates fall, so if you sold early you'd realize a small gain — but at maturity you get exactly what was promised.

- New T-bill auctions: Reprice immediately. The 4-week bill auctioned the Tuesday after a cut will reflect the new policy rate.

If you expect cuts and want to capture today's yields for longer, the CD and the 52-week T-bill both lock them in. The HYSA is the explicit bet that rates stay high or that liquidity is worth the risk of repricing.

The Decision in Four Lines

- Emergency fund under $25K: HYSA. The yield gap doesn't justify the friction.

- Known deadline 3-24 months in a no-income-tax state: CD matched to the deadline.

- Known deadline 3-12 months in a high-income-tax state: T-bill ladder matched to the deadline.

- Six-figure cash bucket, high-tax state, no fixed deadline: Rolling 26-week T-bills. The state-tax exemption plus the no-cap Treasury backing wins on both axes.

The right vehicle changes when the Fed moves, when your state of residence changes, and when your timeline tightens or loosens. The framework above gives you the answer at every step — without re-running the spreadsheet each time rates twitch.

Once you've picked a vehicle, run the actual dollar projections through our compound interest calculator to see how the chosen rate compounds over your specific timeline, then map the contributions through the savings goal calculator if you're building toward a target. If this cash is part of a longer plan, model the bigger picture in the retirement calculator — short-term yield matters less than getting the allocation right across decades.

And if the cash you're parking comes from a paycheck you'd like to keep more of, take 30 seconds in the Pay.thicket.sh take-home calculator to see exactly what hits your account after federal, state, FICA, and benefits — that's the number that funds the HYSA, CD, or T-bill ladder you just chose.

Frequently Asked Questions

Project Your Cash Yield Over Time

Plug your balance and chosen rate into the compound interest calculator to see exactly what your HYSA, CD, or T-bill ladder produces over 1, 5, and 10 years.

Open Compound Interest Calculator →Build Toward a Savings Goal

Model how long it takes to hit a specific dollar target at HYSA, CD, or T-bill rates — with your real monthly contribution.

Open Savings Goal Calculator →